All candidates for federal office, including the presidency of the United States, are required by law to file financial disclosure reports. And although they are not required to do so, ever since the 1970s candidates running for the nation's highest office have been releasing their tax returns to the public as well.

However, a major talking point of the 2016 election season involves Republican candidate Donald Trump's steadfast refusal to release his tax returns, leading to speculation, hoaxes, and elaborate jokes about the issue.

In September 2016, political blogs and forums began bandying about the idea that by President Obama could outflank Trump, because the chief executive possesses the legal authority to request any individual's tax return from the Internal Revenue Service (IRS) for examination:

Fifteen months after he began his campaign and less than two months before Americans go to the polls, Donald Trump is still yet to release any of his tax returns. Despite calls from both Democrats and past Republican nominees, Trump remains defiant to a long-standing bi-partisan tradition. But there’s one person who could render this whole debate moot. One man has the sole authority to order any of Trump’s tax returns be publicly released: President Barack Obama.

The notion that the President could release Trump's tax returns took root deeply and quickly, posed as a question at a White House Press Briefing to Secretary Josh Earnest on 14 September 2016. Earnest was stymied by the question but surmised that President Obama was unlikely to intervene:

Q: A couple questions on the President's comments in Philadelphia about Trump's taxes. Is it fair to take from the fact that he brought this up I believe twice in the speech, that the President believes that it's important or valuable for votes to have information on Trump's taxes, or to see those returns before they go to the polls in November? — under Section 6103G, the President — “Upon written request by the President, signed by him personally, the Treasury Secretary can furnish to the President or to employees of the White House Office the President may designate a return or return information with respect to any taxpayer named in such a request.” And the section goes on to say that as long as you or others have the personal written direction of the President, you’re free to go ahead and release that.

So would the President feel this is so important that he’d be willing to get those returns from the Treasury and make them public if voters really should have this information by November?

A: Well, I’ve not heard of this potential option. I think it is rather unlikely that the President would order something like that. And so if there’s more on this with regard to our position about the interpretation of the statute, we’ll consult the lawyers and let you know ... I think there are a couple of principles here. Certainly one thing that is important and certainly something that’s been prioritized in this administration is making sure that the work of the IRS is not affected with even the appearance of political influence. And in this regard, obviously the President has made clear that he’s a strong supporter of Secretary Clinton in the presidential race.

I think the second thing, though, Josh, is this — no other presidential nominee in either party has ever been compelled to release their tax returns. They’ve all done so voluntarily. There’s been no reason to resort to obscure sections of the tax code to try to find a reason to force them to release these tax returns. Candidates for at least a generation now — again, in both parties — have voluntarily released these tax returns and made them public.

And the President feels — I think made the point yesterday that the fact that there is one nominee who won’t voluntarily make them public I think is something the American people should consider as they evaluate their choices for President of the United States.

While it seems likely that President Obama could obtain and release Donald Trump's tax returns, whether he could so legally is not so certain. Under Section 6103g of the Internal Revenue Act of 1954, the President may submit a request for the IRS to provide him (or a designated employee) with "return information with respect to any taxpayer." That request must include "the specific reason why the inspection or disclosure is requested":

(g) Disclosure to President and certain other persons

(1) In general

Upon written request by the President, signed by him personally, the Secretary shall furnish to the President, or to such employee or employees of the White House Office as the President may designate by name in such request, a return or return information with respect to any taxpayer named in such request. Any such request shall state —(A) the name and address of the taxpayer whose return or return information is to be disclosed,

(B) the kind of return or return information which is to be disclosed,

(C) the taxable period or periods covered by such return or return information, and

(D) the specific reason why the inspection or disclosure is requested.

However, that section of the U.S. Code only authorizes the President to obtain and examine tax returns, not to publicly disclose them. Presumably the rules regarding confidentiality stated at the beginning of that section would still apply, even to the President:

Returns and return information shall be confidential, and except as authorized by this title —

(1) no officer or employee of the United States shall disclose any return or return information obtained by him in any manner in connection with his service as such an officer or an employee or otherwise or under the provisions of this section.

A separate IRS document [PDF] reiterates that the bulk of tax records are considered highly confidential, noting that a President could access them but:

Unless otherwise specifically authorized, tax returns and return information may not be disclosed by individuals who have access to them. IRC 6103 defines the terms "tax return" and "return information" very broadly to include just about everything concerned with an individual's or organization's reporting and paying of federal taxes. However, "tax returns" and "return information" may be disclosed under limited circumstances.

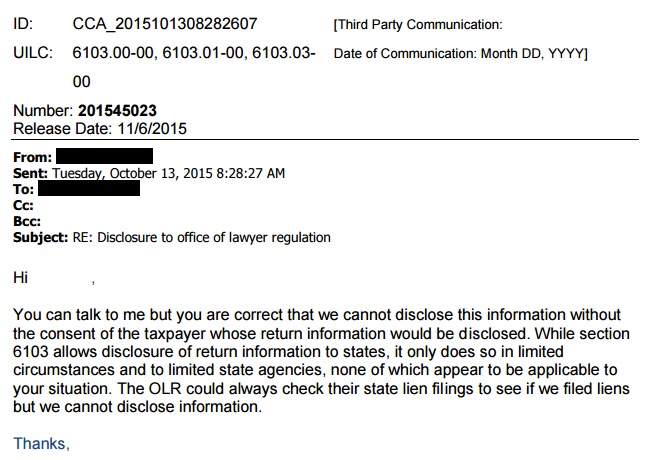

Various IRS rulings pertaining to the disclosure of information under numerous similar tax code clauses uniformly cite parties (such as states) granted the legal ability to request such information [PDF], but those documents also stipulate that the taxpayer's consent is required for any other disclosure:

Additionally, even if he requested but didn't release Donald Trump's tax returns, the President would still be required to file a report stating that he had done so and explaining the reason(s) why:

Within 30 days after the close of each calendar quarter, the President and the head of any agency requesting returns and return information under this subsection shall each file a report with the Joint Committee on Taxation setting forth the taxpayers with respect to whom such requests were made during such quarter under this subsection, the returns or return information involved, and the reasons for such requests.

Given that Donald Trump is under no obligation to release his tax returns, and President Obama likely has no legal authority to publicly release them (or justification for examining them), it's not likely that we'll be seeing them unless the GOP candidate himself chooses to show them to us.