An item about a collection of U.S. tax increases which were supposedly enacted as of 1 January 2016 due to the provisions of the Affordable Care Act (commonly known as "Obamacare") was circulated widely at the beginning of 2016, but it was merely an updated version of identical claims circulated in previous years that set 2014 or 2015 as the imposition date for those tax increases:

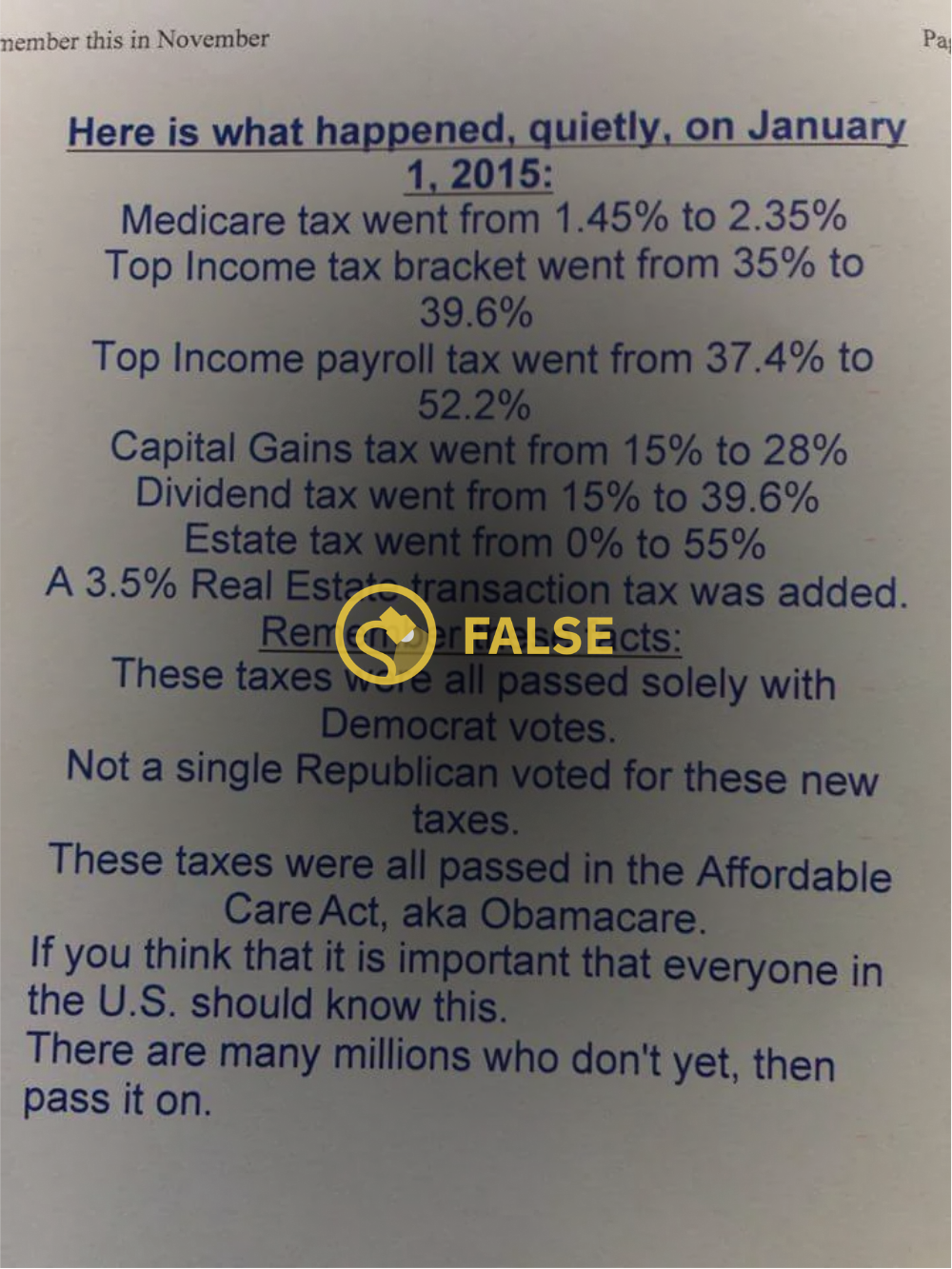

Although the tax increases listed in this item did come to pass, they took effect at the beginning of 2013 (not 2014 or 2015 or 2016), were completely unrelated to the Affordable Care Act, applied only to very high-income earners, and have been overstated in this list. These tax hikes were enacted through the passage of the American Taxpayer Relief Act of 2012, a compromise bill pushed through Congress as a partial resolution to the then-looming "fiscal cliff" crisis. Under the provisions of that bill:

- The top marginal federal income tax rate increased from 35% to 39.6%

- The top marginal tax rate on long-term capital gains increased from 15% to 20% (not 28%).

- The top marginal tax rate on dividends increased from 15% to 20% (not 39.6%).

- Estate taxes increased from 35% of an estate's value in excess of $5,120,000 (in 2012) to 40% of the value above $5,340,000 (in 2014).

It's important to note that the increase in marginal tax rates for federal income tax, capital gains, and dividends affected only those persons with taxable incomes over a $400,000 (single)/$450,000 (married) threshold. It's also important to note that the previous estate tax rate of 0% was a special rule that applied only to the estates of persons who died in 2010 (the estate tax has since been increased to 35% for those who died in 2011 and 40% for those who died in 2012 and thereafter), and even today an estate tax filing is required only for estates with gross assets in excess of $5 million (indexed for inflation).

The tax rate for dividends has also not increased from 15% to 39.6%: it appears someone has confused qualified dividends with nonqualified dividends. Qualified dividend earnings are tax-free for those in the 10% and 15% brackets, taxed at a 15% rate for those in the 25% up to 35% tax brackets, and taxed at a 20% rate for higher income taxpayers whose income surpasses the 35% tax bracket. Nonqualified dividends only are taxed as ordinary income. (Theoretically, a taxpayer with nonqualified dividend earnings who reached the top marginal federal income tax rate would be paying 39.6% tax on those earnings, but that's a condition that only applies to persons earning over several hundred thousand dollars per year.)

The list's reference to an "income payroll tax" increase from 37.4% to 52.2% is something of a mystery, as this is not a standard term for any type of government income- or payroll-related tax. The only adjustment to payroll-related taxes resulting from the American Taxpayer Relief Act of 2012 was that a two-year old cut to payroll taxes which had previously reduced the rate from 6.2% to 4.2% for 2011 and 2012 was not extended.

Additionally, this item's coda claiming that "not one Republican voted to do these taxes" is completely false. The American Taxpayer Relief Act of 2012 passed Congress by a margin of 89-8 in the Senate with 40 Republican votes in favor, and a margin of 257-167 in the House with 85 Republican votes in favor. (The original claim undoubtedly refers to the House or Representatives' voting in 2010 to pass the health-care reform bill without a single Republican vote in favor, but that association is moot because, as noted, the tax increases listed above had nothing to do with that bill.)